Media Clips

Source: International Tax Review

Cultural nuances could account for tax advisers' perceived poor cost management, a local partner told ITR

Read more 'What Corporates Want' reports here

External tax advisers in Southeast Asia are ranked the lowest in the world when it comes to managing costs and budgets, according to exclusive data from ITR+'s latest What Corporates Want report.

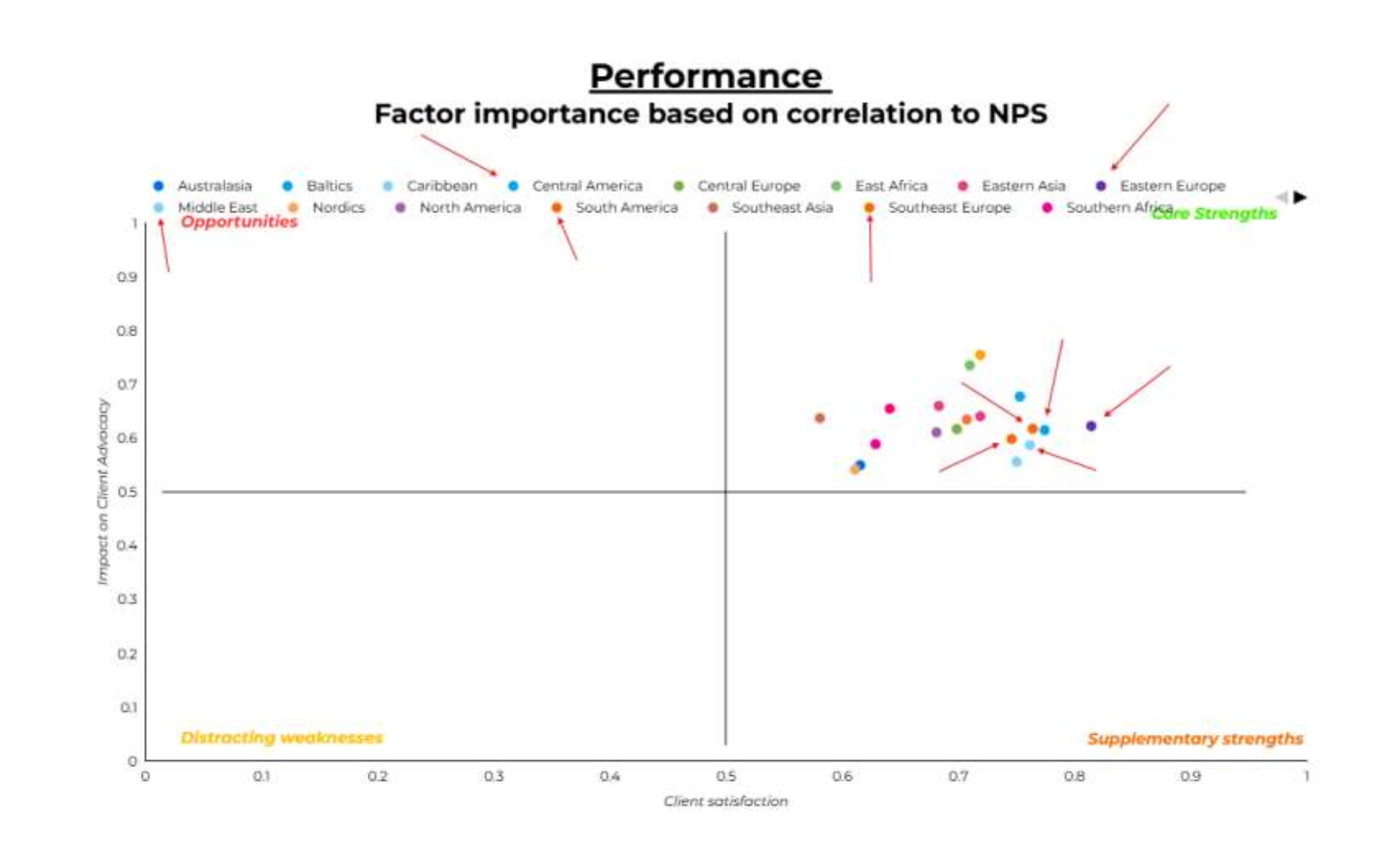

At the other end of the scale, Eastern Europe and Central and South America were among the highest- rated jurisdictions for budgeting.

In-house counsel were asked to rate several factors for their impact on client advocacy on a scale from o to 1, with o being the least important and 1 being the most important.

Clients were also asked, using the same scale, to score their satisfaction with advisers across the factors.

A total of 1,856 in-house tax counsel responded to the surveys.

You can find all our previous reports, which covered topics including client management and corporate social responsibility, on our What Corporates Want hub page.

This report focuses on fees and billing, and the specific sub-factors of managing costs and budget and value for money.

In terms of managing costs, Eastern European advisers came out on top, with a client satisfaction score of 0.81 out of 1. Central America (0.77), and Southeast Europe and the Middle East (both 0.76) took the next leading spots.

Despite these ringing endorsements, nearly all the client satisfaction scores for managing costs were offset by middling to low client impact scores.

In Eastern Europe, for example, the 0.81 satisfaction score paled against the 0.62 client impact rating.

This gap was also pronounced in South America, where in-house counsel gave their external advisers a strong 0.74 out of 1 on client satisfaction but just a 0.59 in terms of impact.

Daniel Cordeiro, group tax manager at Brazilian aerospace company Embraer, tells ITR that this finding “is quite representative of what happens in real life”.

However, he insists that he would rate managing costs as either a 0.7 or an 0.8 on importance, significantly higher than the 0.59 score given by his peers.

"With pressure across the board in virtually all organisations in terms of budget and results, ensuring your advisers can stay within the allocated limits is quite relevant for in-house managers," Cordeiro says.

Despite this, he believes the survey findings reflect a realistic view of budgeting taken by in-house counsel.

"One of the reasons for the gap between the two indicators could be that in certain projects, especially strategic ones which could bring in tax credits or other revenues for the company, it is more important to obtain results.

"Even if some overrun occurs, it's more important to get the result than delaying or preventing the work just to avoid incurring additional expenses."

Allan Fallet, a tax partner at law firm Duarte Garcia, Serra Netto e Terra in São Paulo, says the lower importance rating for budgeting “suggests a nuanced distinction between cost management as a process and its perceived strategic significance”.

"Managing costs involves estimating, allocating, and controlling expenses to prevent budget overruns," he explains. "This requires a structured approach where projected costs are calculated during the planning phase and approved before execution."

Fallet also argues that there is a distinction between cost estimation and budgeting. The former, he asserts, is a "preliminary calculation based on known market indices and serves as a reference point" but shouldn't be used as a formal pricing tool.

"Budgeting, on the other hand, is a more detailed and structured financial plan,” Fallet adds.

Ultimately, Fallet believes that the survey results indicate that in-house counsel simply have more important factors to consider.

"This gap in perception may stem from the fact that while external tax advisers excel at financial discipline, in-house teams may prioritise other factors, such as technical expertise, regulatory compliance, or business alignment," he concludes.

At the other end of the scale, there was no sub-region where external advisers were rated lower at managing costs than Southeast Asia.

Advisers in the region were scored just 0.58 out of 1 on the satisfaction scale, against a 0.63 client impact rating, indicating that in-house counsel in Southeast Asia are slightly under-served on this metric.

Other low-scoring regions for satisfaction included the Nordics (0.61), Australasia (0.61) and Southern Africa (0.62), but these were all offset by even lower client impact ratings. This suggests that budgeting is a lower priority in these regions.

To understand the results in Southeast Asia, ITR spoke to Singapore-based tax adviser Pierre Vanrenterghem of advisory firm RBA, who argues that cultural nuances are at play.

"I've worked for firms in Europe and Asia and, in my experience, the processes for managing budgets and costs are similar in both regions," he says.

"However, it needs to be added that Asian clients are generally less accustomed to hiring external advisers. While our clients in Europe have always been surrounded by lawyers and tax advisers for generations, it is a relatively new service in Asia."

Vanrenterghem asserts that this can lead to advisers in Southeast Asia applying European standards of services but also fees, without correctly considering the client's situation.

"The client is not used to paying for a service that is, by its nature, intangible,” he concludes.